“Let no one think that flexibility and a predisposition to compromise is a sign of weakness or a sell-out” Paul Kagame

Life is full of surprises. I am pretty certain that UK Prime Minister Theresa May would have preferred not to have been so surprised by the reaction to her Brexit preferences in Salzburg, during late September. However – as with life – it is how you react that really matters.

Sorry no cherries today

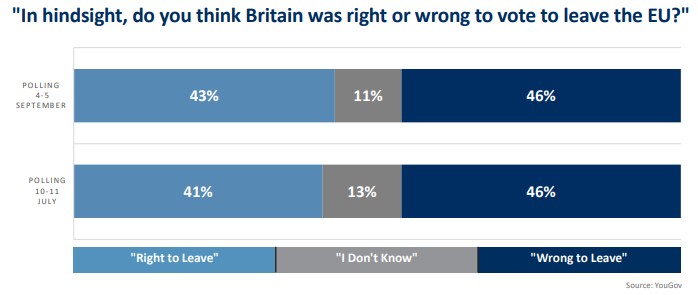

So how do you react? Theresa May’s grumpy press conference followed Donald Tusk’s now infamous ‘sorry no cherries today’ Instagram reflecting, if we did not know already, that the whole Brexit process has been a series of forward steps followed by backward one. What was most striking to me however was the sharp distinction between the hope of just a few days prior to the Salzburg summit, when talk of a November – or even possibly an October – final deal was apparent. With time ticking away these scenarios appear less likely… so can a compromise be reached that will solve the Irish border and general future trade relationship, and sell it to Parliaments and underlying citizens?

Why compromise?

What is the logic for striking a compromise deal? Well it has to be centred on trade and its contribution to economic activity. After all, from a UK perspective, exports of goods and services to other European Union (EU) countries were worth £274 billion in 2017 (over 40% of total UK exports), while exports from the rest of the EU to the UK were worth about £341 billion. No deal does not stymie this completely, but every new frictional cost or barrier is a hindrance or a loss that has to be overcome or sourced from elsewhere.

Answering the border question

Common sense and political/economic decision-making are rarely one and the same thing and the world of Brexit is replete with emotional, instinctive thinking. The Irish border question is clearly one of these issues. Fortunately, the full weight of the history underlying this question is not apparent and policymakers need to just concern themselves in avoiding a ‘hard border’. Could technology take up the strain as with so many other elements in our modern lives, tracking goods to their final destination? Certainly a next generation version of the current fluid Swedish-Norwegian border (average wait time nine minutes) or US-Canadian border (average wait time just under sixteen minutes – assuming Fast and Secure Trade Program membership) could exist for the Irish border.

It is clearly not perfect but it is should be good enough to satisfy enough people initially to get something through and agreed.

Chequers or no deal

And then there is trade. The careful compromise of the ‘Chequers deal’ and its facilitated customs arrangements looks unlikely to politically hold up, and the ongoing EU’s binary focus (outside ‘no deal’) on either something like the current status quo or an off-theshelf existing ‘Canada-style’ deal seem at face value to be the only options on the table (and the latter causes Irish border challenges). Clearly, here is where UK politics kicks in, but if you take away those with very firm and vocal views, the closeness of the 2016 referendum – especially when combined with a UK Parliamentary majority in favour of ‘remain’ – indicates the most likely outcome is for Brexit… but only in a soft and transitional manner. With a twenty-one month transition period already on the table for the post end of the March 2019 period, efforts have already been made to try and avoid an aggressive cliff edge.

Now some will say that such a scenario is impossible because the current UK government will be unable to muster sufficient support on its own benches, however, remember the general, average Parliamentary view, which is likely to be in favour of a soft Brexit at most. At some point – despite obvious party politicking incentives – such a huge constitutional matter cuts across party boundaries irrespective of which political party nominally has a majority (or not). Meanwhile, the trouble with the rationale for a second referendum is that any question gets hijacked and is unclear in a transitional scenario.

What happens next?

What we have now is clearly an impasse, but not an unassailable one. Brexit, with its step forward and backwards, remains tricky, unclear and newspaper headline catnip. It has held back the Pound, UK domestic shares and even the broader continuing European Union. But from the current desperately mixed sentiment backdrop, any resulting deal will lift all these boats in a potentially tradeable manner for investors.

But – as we started this piece – what happens beyond March 2019 depends on how consumers, businesses and politicians react to any deal. Forging a deal is important but with the backdrop of a competitive, evolving world, what everyone does with it matters much, much more. In short, even with compromises, challenges and opportunities exist with the Brexit debate.

You can read more articles from Chris Bailey and the Raymond James Investment Strategy Committee in the October edition of Investment Strategy Quarterly

*An affiliate of Raymond James & Associates and Raymond James Financial Services

DISCLAIMER: The information contained in this article is for general consideration only and any opinion or forecast reflects the judgment of the Research Department of Raymond James & Associates, Inc. as at the date of issue and is subject to change without notice. Past performance is not a reliable indicator of future results.

You should not take, or refrain from taking, action based on its content and no part of this article should be relied upon or construed as any form of advice or personal recommendation. The research and analysis in this article have been procured, and may have been acted upon, by Raymond James and connected companies for their own purposes, and the results are being made available to you on this understanding.

Neither Raymond James nor any connected company accepts responsibility for any direct or indirect or consequential loss suffered by you or any other person as a result of your acting, or deciding not to act, in reliance upon such research and analysis. If you are unsure or need clarity upon any of the information covered in this article, please contact your wealth manager.

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|