Chris Bailey, European Strategist, Raymond James Euro Equities*

“There cannot be a crisis next week. My schedule is already full” Henry Kissinger

The Eurozone has been in a troubled mode during 2018. The sight of German Chancellor Angela Merkel – Europe’s longest serving and most important elected politician – struggling to not only put together but also to keep together a workable coalition has encouraged more commentators to write the political and economic obituary of the Eurozone.

Certainly international investors have voted with their feet in the past six months, with outflows at levels not seen since the days following the UK’s European Union referendum in June 2016. Merkel’s political scrambling has been accompanied by the surprise formation of a populist tinged government in Italy, a change of leadership in Spain after a long-running corruption scandal and underwhelming economic data.

So, has the hope of 2017 – following the election of an energetic new French President committed to reform and change – gone forever? Despite all the above, there has been some positive change and most of this has been centred upon the efforts of Emmanuel Macron. The French President has broadly lived up to his promise to introduce much needed economic, labour market, taxation and entrepreneurial reforms plus rebuild national confidence. And Macron’s energy has not been the only encouraging regional positive: Greece is finally on the cusp of exiting its economic support programme, meanwhile the European Central Bank has set a date at which it intends to stop adding to its quantitative easing stimulus – although interest rates are set to remain in negative territory for at least another year.

In short, the hopes that a revitalised Franco-German leadership could push an attractive Europe 2.0 vision that could excite the pan-European electorate, has been unsettled by shorter-term political, economic and social considerations led – especially in Italy and Germany – by issues such as immigration and inequality. However, the history of the Eurozone has been that the most difficult and sometimes contentious decisions have generally been taken when political backs are against the wall. And there is the scope for 2018 to still be one of those years.

June’s much-anticipated Summit of European leaders was ultimately hijacked by some of the shorter-term considerations noted above but, it is to the Eurozone’s credit, that some progress was made and agreements reached. The new EU budget, stretching deep into the 2020s, deepens the Eurozone’s regional redistribution capabilities – absolutely essential for the effective working of a single currency zone (as the United States would attest). More regional distributions towards southern Europe offers the scope of ‘cash for reforms’ style deals, but at the moment it is still just a hope, with further details to be worked out by the end of the year.

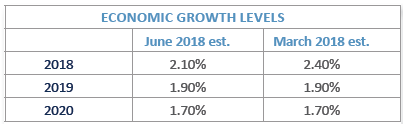

Economic realities at two levels will be critical influences over the balance of the year. The first is whether the Eurozone economy can start to surprise again after a first quarter badly hit by unhelpfully poor weather and tough comparisons. Regional economic growth rates remain below medium-term aspirations but an economic recovery is still taking place, which includes the best rate of bank lending growth since before the global financial crisis. Given, as aforementioned, interest rates for the Eurozone are still currently at negative levels, this should be no huge surprise, but more jobs and some wage growth can only be a positive at-the-margin for the whole region.

The second economic reality rests with the region’s third largest economy: Italy. As the coalition government is fast learning, it is easier to talk than govern, and further signs that the country is embracing change and reform as a committed member of the Eurozone, can only help confidence towards the whole region. High debts and a still strained banking system – as the Greeks would agree – is best managed with the help of the Eurozone authorities. A pragmatic Germany and an energetic France could still yet find a workable formula for a future Eurozone that remains troubled but not, by any means, on its deathbed. For investors today there remains more opportunity than threat.

Source: European Central Bank

You can read more articles from Chris Bailey and the Raymond James Investment Strategy Committee in the July edition of Investment Strategy Quarterly

*An affiliate of Raymond James & Associates and Raymond James Financial Services

DISCLAIMER: The information contained in this article is for general consideration only and any opinion or forecast reflects the judgment of the Research Department of Raymond James & Associates, Inc. as at the date of issue and is subject to change without notice. Past performance is not a reliable indicator of future results.

You should not take, or refrain from taking, action based on its content and no part of this article should be relied upon or construed as any form of advice or personal recommendation. The research and analysis in this article have been procured, and may have been acted upon, by Raymond James and connected companies for their own purposes, and the results are being made available to you on this understanding.

Neither Raymond James nor any connected company accepts responsibility for any direct or indirect or consequential loss suffered by you or any other person as a result of your acting, or deciding not to act, in reliance upon such research and analysis. If you are unsure or need clarity upon any of the information covered in this article, please contact your wealth manager.

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|