By Jeff Saut, Chief Investment Strategist RJF, Tuesday 10 September 2018

The brilliant Peter Bernstein (author, historian, and economist) once wrote:

After 28 years at this post and 22 years before this in money management, I can sum up whatever wisdom I have accumulated this way: the trick is not to be the hottest stock-picker, the winning forecaster, or the developer of the neatest model; such victories are transient. The trick is to survive. Performing that trick requires a strong stomach for being wrong, because we are all going to be wrong more often than we expect. The future is not ours to know. But, it helps to know that being wrong is inevitable and normal, not some terrible tragedy, not some awful failing in reasoning, not even bad luck in most instances. Being wrong comes with the franchise of an activity whose outcome depends on an unknown future. Maybe the real trick is persuading clients of that inexorable truth.

So, we were on Fox Business News last Friday with the sagacious Neil Cavuto. He noted President Obama’s comments that the economic recovery was created by him, but that President Trump is taking all the credit for it. Neil then asked us, “Do you believe that?” We responded, “That is a fair point, but we think the Fed should be given a lot of the credit for keeping us from a depression.” A few minutes later he asked what we thought of the stock market. We responded (as paraphrased):

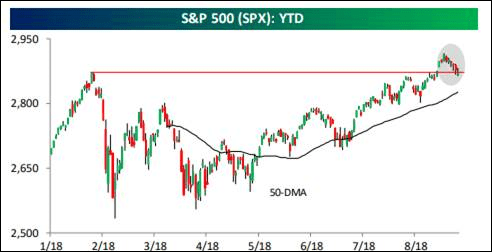

Well, we have had a pretty good call on the equity markets this year. We recommended raising some cash in late January, suggested putting that money back to work after roughly an 11% decline by the S&P 500 (SPX/2871.68) near its February 9 low and we were looking for new all-time highs. Mission accomplished! Subsequently, two weeks ago tomorrow, after tagging those new all-time highs, we wrote that the SPX was likely going to stall, but we did not think the SPX would trade below its 2890 – 2900 support level.

And as we said to Neil, “That near-term trading finesse ‘call’ was wrong.” That said, we remain undeterred about the secular bull market that has years left to run. Neil was quite gracious, inferring we should not be so hard on ourselves.

Being wrong and admitting it, what a novel idea, yet as Bernstein states, “It helps to know that being wrong is inevitable and normal, not some terrible tragedy, not some awful failing in reasoning, not even bad luck in most instances. Being wrong comes with the franchise of an activity whose outcome depends on an unknown future.” Indeed, the real trick is to be wrong quickly for a de minimis loss of capital.

Consequently, we were surprised when the SPX traded to an intraday low of ~2864 on Friday as the market was also surprised by the potential for an additional $267 billion in tariffs on Chinese goods. To do the math, currently there are 25% tariffs on $142 billion of goods by China and the U.S. Last year the total relationship of goods traded was around $635 billion. Accordingly, some 22% of the total goods trading relationship is being affected ($142/$635 = 22%). However, that is not the right way of looking at it. What should be considered are the 25% tariffs on $142 billion worth of goods, or $35.5 billion. Then using the same formula yields an overall impact of only 5.6% of the total goods trading relationship (25% of $142 billion equals $35.5 billion; $35.5 billion divided by $635 billion equals 5.6%). Yet, if the President does indeed impose a 25% tariff on an additional $267 billion worth of Chinese goods the equation changes dramatically. Whether this happens remains to be seen, but clearly it is going have an impact on the various markets.

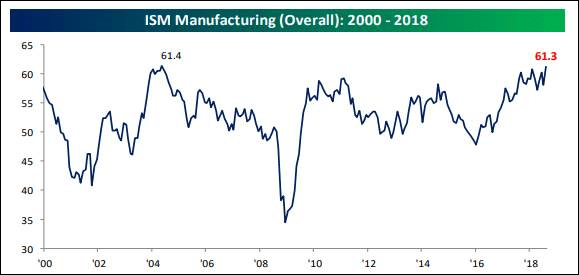

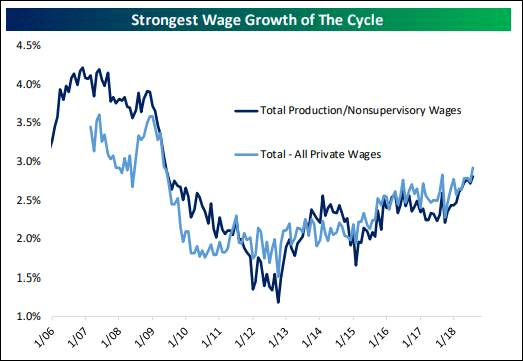

Moving on, the start of September for the SPX was the worst since 2015. For the NASDAQ (-2.55%) it was the worst since September 2008. Given that backdrop it was no surprise the Advance-Decline Line failed to register another new all-time high, yet the breadth for the week was not too bad. While last week’s decline surprised us, it should be noted that all the SPX did was pull back to a support level (chart 1 on page 3). Looking at the FAANGs, however, is troublesome since these previous market leaders have weakened noticeably. Also troublesome is the emerging market (EM) space, which has declined by some 20% (chart 2). In fact, this is the longest such decline by the MSCI Emerging Market Index, without a 10% rally, in decades. Meanwhile, the underlying U.S. economy remains strong with last week’s ISM Manufacturing Index printing at 61.3. Worth mention is that the ISM Manufacturing Index is at its highest level in quite some time and history suggests it will peak about 35 months before a recession begins (chart 3 on page 4). Moreover, history shows that a recession tends to happen a full two years after the yield curve inverts (we do not think the 2 – 10 year T’Note yield curve is the right curve to look at). Clearly, the economy is strong and wages are picking up (chart 4). Therefore, investors will put on “rabbit ears” for this week’s inflation numbers as a number of companies have already reported the higher prices they are paying for raw input materials.

For the week, of all the indices we monitor only the D-J Transportation Average (+0.39%) and the D-J Utility Average (+0.99%) were up on the week. The same can be said for most of the commodities we watch, as well as most of the currencies, as the U.S. Dollar Index rallied (+0.24%). It should be mentioned that the number of S&P 500 stocks above their respective moving averages currently resides around 75%, for the highest reading since late February price peak, implying the stock market was pretty overbought early last week. This overbought condition is reinforced by the 14-week Stochastic Model. As for our models, the larger than expected weekly decline of last week caused our various trading models to rebuild their internal energy. Still, those models “look” for the equity market to continue the “big stall” that we wrote about two weeks ago.

The call for this week: The D-J Transports made a new all-time high recently, which has not been confirmed by a new all-time high in the D-J Industrials. That, as of now, is a Dow Theory upside non-confirmation that we will be monitoring in the sessions ahead. This week will also be the anniversary of the Lehman bankruptcy (9/15/08); oops. And don’t look now, but the old stock market saw “sell on Rosh Hashanah (which began last night) and buy on Yom Kippur (sundown Tuesday 9/18/18)” has not really played much in recent years, but it is worth a mention. Speaking to the Buying Power and Selling Pressure indices, Buying Power has seen a slight softening since late July, while Selling Pressure has experienced a slight increase. This does not meaningfully impact our bullish “call.” As our friend Leon Tuey wrote us late last week:

Earlier this year, because of the market’s oversold condition and ideal sentiment backdrop (global panic), investors were advised to re-deploy cash. I (dictated by hard evidence) concluded that the market bottomed and the bull market had resumed. As expected, the market surged and last week, except for the Dow Jones Industrial Average, the market reached a new record high. Why is the market pausing this week? From their respective lows this year to last week’s close, note how the various market measures and the Advance-Decline Lines have performed:

S&P 500 Index, +12.1%; S&P Mid-Cap Index, +12.3%; NASDAQ Composite Index, +18.0%, Russell 2000 Small-Cap Index, +21.3%, and S&P Small-Cap, +21.7%.

Indeed, while the SPX’s pullback was deeper than we expected on a very short-term trading basis (read: wrong), it has not deterred our secular bull market “call” that should last for many years. The markets have also morphed into an earnings-driven secular bull market since mid-2015, and we identified it back then. In addition to that, we have also moved into a credit-driven bull market as huge amounts of capital (offshore profits repatriation, M&A, share repurchases, etc.) have poured into the scene. Importantly, pension/endowment/sovereign wealth/funds desperately need to play “catch up” because of lagging returns (read: too cautious) making their targeted return assumptions well below their trailing results. This morning the preopening S&P 500 futures are better by some 10 points as no new tariffs have been announced.

Chart 4

Source: Eikon

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|