By Jeff Saut, Chief Investment Strategist RJF, Monday 02 July 2018

“Having missed most of the bull market over the past nine years, a great many investors have pronounced that we are now, at last, in a bear market. I do not know. What I do know is that our companies are doing better than I could have ever hoped, their current prices seem reasonable, and their futures look very bright.”

. . . Frederick “Shad” Rowe, Greenbrier Partners, June letter

Our friend Shad goes on to write in his June letter:

As bulls and bears battle it out, stock market volatility increases, rattling our teeth and shaking our brains, we go over again and again what we are trying to do. As we have repeated ad nauseam, we attempt to invest at reasonable prices in publicly traded companies that conduct their businesses better, faster, and cheaper than their competition and whose primary motivation is to do things for rather than to their customers. We also look for that something extra that sets our companies apart. That something extra is company culture.

Of interest is that in Shad’s “investment model” 95% of his portfolio is in just 12 stocks. We call that “concentration,” and I actually like concentration. Concentration is how you get rich! Diversification is how you stay rich. You can look at just about any billionaire and see that’s how they got rich, by being “concentrated” with their investments. My own approach to investing is actually quite simple.

Personally, I start with a base position of actively managed mutual funds, but not just any fund. The funds I want to own are the ones where I know the portfolio manager. Importantly, I don’t monitor the price of funds I own, except at tax time, because I’m confident over the long run my pal Tom O’Halloran at Lord Abbett, who manages the Lord Abbett Growth Leaders Fund, is going to make me money. A couple of other such names would be my friend Mary Lisanti, who manages the Lisanti Small Cap Growth Fund, and Amy Zhang, who manages the Alger Small Cap Focus and the Alger Small Cap Growth Strategies funds. If you want to be impressed, check out Mary and Amy’s performance year to date.

So, for my own investments, I start with a base of mutual funds, but because I talk to these boys and girls that have to put money to work, I hear a bunch of good ideas. Now in a past life I have been on a trade desk, a stockbroker, analyst, portfolio manager, director of research at five different firms, and the head of capital markets at three firms. Accordingly, when Ron Baron (Baron Capital and one of the best stock pickers I know) gives me an idea, I can spend some time on Factset looking at the technicals, fundamentals, ownership, etc. and decide if I want to start buying the stock. And that, ladies and gents, is how I attempt to add alpha (read: outperformance). As stated, my personal approach to investing is really simple, but it works.

Moving on to the equity markets, as we wrote in last Friday’s Morning Tack:

The intermediate-term model remains on a “buy signal,” while the short-term model is basically trendless, implying what we have been through is just a normal/standard retracement move despite the recent downside “heart attack.” As often written, following a stock market heart-attack the equity markets typically need to convalesce for a few sessions before regaining their poise; and, it manifestly has been a few sessions. Looking at the “internal energy” model shows there is plenty of energy to make a rally attempt have a sustained “leg” to the upside. Accordingly, it would be surprising to Andrew and me to see the SPX comeback down to yesterday’s intraday low of 2691.99.

Our work suggests the equity markets are gathering enough energy, and momentum, to permit a dash to new all-time highs and then keep right on pushing higher. Interestingly, almost NOBODY is expecting this to occur. Most continue to look for a decline, or at best a range-bound stock market. We do not believe it, but must admit we were surprised by the additional tariff news and the concurrent stock market one-session “heart attack,” which interrupted the upside rhythm of the market we had expected. However, that heart attack is now in the rearview mirror.

Plainly energy stocks, and crude oil prices, were in the forefront of last week’s trading as WTI crude leaped 8.08% (spot month). Readers of these missives know that for many months we have been favorable on the energy complex and have recommended tilting portfolios accordingly (Chart 1). Over the weekend President Trump tweeted that he has asked Saudi’s King Salman to increase oil production by some two million barrels a day. Therefore, it will be interesting to see how crude oil prices act today. If oil prices decline, with a concurrent decline in share prices, there are two stocks that are favorably rated by our energy analysts and screen well on our algorithms: Occidental Petroleum (OXY/$83.68/Outperform) and Marathon Petroleum (MPC/$70.16/Strong Buy) are offered for your consideration.

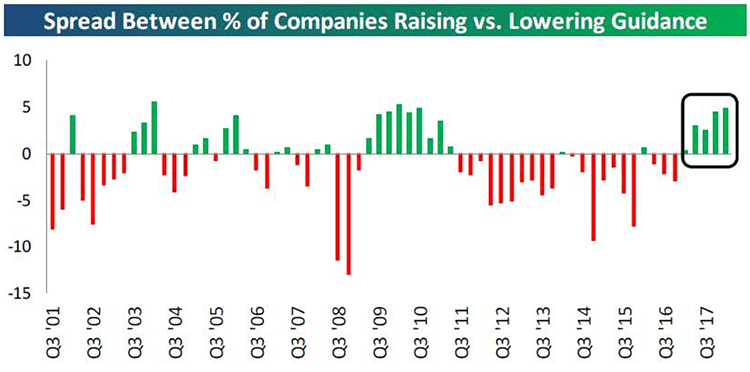

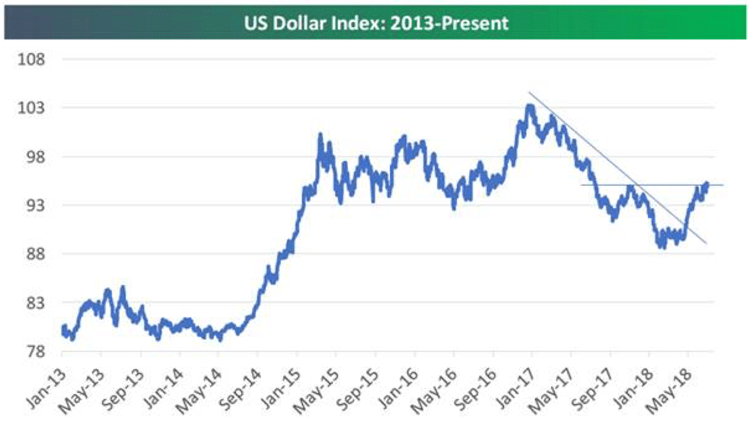

Turning to earnings, as we approach yet another earnings season, we believe the same folks that told us 1Q18 represented “peak earnings” are going to be proven wrong once again. Just look at the attendant chart of the spread of the percentage of companies raising, versus lowering, forward earnings guidance (Chart 2). As our friend Bob Pisani notes, “S&P 500 earnings are not peaking yet. Quarter 2 estimates earning to be up 20.3%, Q3 up 23.1%, and Q4 better by some 20.1%.” Another thing we will be watching closely will be the U.S. Dollar Index (DXY/94.47), which looks to us as if it attempting to stage another leg to the upside (Chart 3).

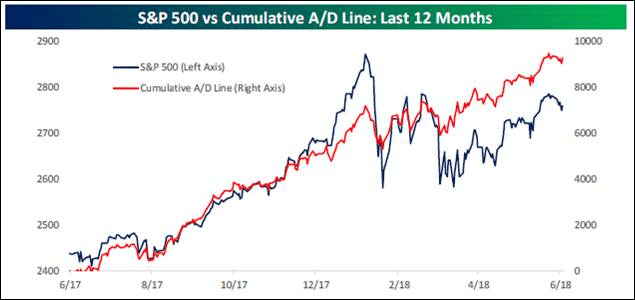

The call for this week: While it didn’t happen last week the recent new all-time highs in the small/mid-cap indices, as well as the Advance/Decline Line, indicate the bull market is alive and well. Moreover, as the indispensable Lowry Research Corporation writes:

At the time of the June 12th high, Buying Power was at a new recovery high while Selling Pressure was at its lowest level in over 70 years, indicating a healthy expansion in Demand and contraction in Supply. Short-term Demand was also strong, as our Short Term Index reached its highest level since early 2011. And, as of the June 12th high, measures of market breadth all indicated a healthy primary uptrend. Not only was our Operating Companies Only (OCO) Adv-Dec Line at a new all-time high, but the OCO and S&P Large, Mid and Small Cap Adv-Dec Lines was each at a new all-time high. In fact, the OCO and S&P Mid and Small Cap Adv-Dec Lines recorded new all-time highs again on June 20th.

This morning, however, the preopening S&P 500 futures are off some 13 points at 5:31 a.m. due to: DJT’s EU sanctions over Iran tweet, Canada’s retaliatory tariffs, Germany’s Merkel possible fall; and Obrador, an anti- DJT Marxist is set to win the Mexican presidency.

Chart 3

Source: Bespoke Investment Group

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|