By Jeff Saut, Chief Investment Strategist RJF, Monday 14 May 2018

Today, we revisit the military preparedness question following President Trump’s nearly $700 billion military budget to attempt to make our military readiness better. We think the recent weakness in the defense sector stocks provides an interesting entry spot for investors. Indeed, many of the defense stocks have collapsed since their mid-April all-time highs. Concurrently, the iShares U.S. Aerospace & Defense ETF (ITA/$198.47) has pulled back. Believe it or not, the defense stocks are not just, well defense stocks, but technology stocks, as well. Take Lockheed Martin’s secretive Skunk Works division. As Wikipedia writes:

Skunk Works is an official pseudonym for Lockheed Martin’s Advanced Development Programs (ADP). It is responsible for a number of famous aircraft designs, including the U-2, the Lockheed SR-71 Blackbird, the Lockheed F-117 Nighthawk, Lockheed Martin F-22 Raptor, and the Lockheed Martin F-35 Lightning II, which are used in the air forces of several countries. The designation “skunk works” is widely used in business, engineering, and technical fields to describe a group within an organization given a high degree of autonomy and unhampered by bureaucracy, with the task of working on advanced or secret projects.

Pretty much for this entire nine-year bull market, we have favored Technology and considered the defense stocks to be technology stocks “in drag” with many of them selling at cheaper valuation metrics than the best known tech stocks. The other sector we have really liked is the Financial sector. To that point, we recently met with Anton Schutz, the portfolio manager of the RMB Mendon Financial Services Fund (RMBKX/$46.70). We met him at the Ocean Reef Club near the top of the Florida Keys. After spending a few days with him, and swapping stock ideas, we became very impressed with his investment model. His fund seeks capital appreciation and pursues that goal by investing at least 80% of net assets in the common stocks of U.S. companies in the financial services sector, but primarily in small capitalization stocks (an under-owned space). Anton invests in companies with strong management teams, sound financial practices, and a defensible business niche. His focus is on firms with sustainable growth in earnings and revenue and strong cash flows and in identifying undervalued equities that are temporarily distressed and, therefore, have merger and acquisition potential. As a sidebar, Anton is friends with our pal David Ellison who manages the Hennessy Small Cap Financial Fund (HSFNX/$24.99), which I own. In the current market cycle, we like the “small-cap” space for numerous reasons and would note that the S&P Small Cap 600 traded to new all-time highs last week.

Moving on to the stock market, the most important chart of last week is the Cumulative Advance/Decline Line chart, which made new highs (Chart 1 on page 2). As Bespoke Investment Group writes:

One of the most bullish aspects of the market throughout the sell-off from the January highs right up through Friday has been the S&P 500’s cumulative A/D line. We’ve highlighted the strength in this indicator a number of times in the last three to four months, but as the chart illustrates, since the S&P 500’s peak in late January, the cumulative A/D line has made three new highs now.

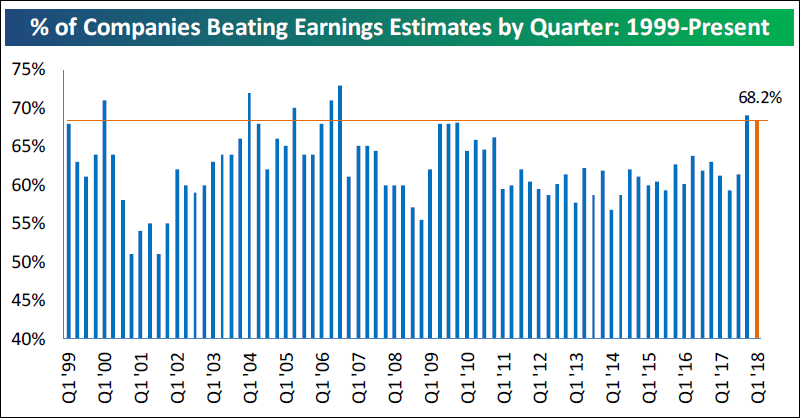

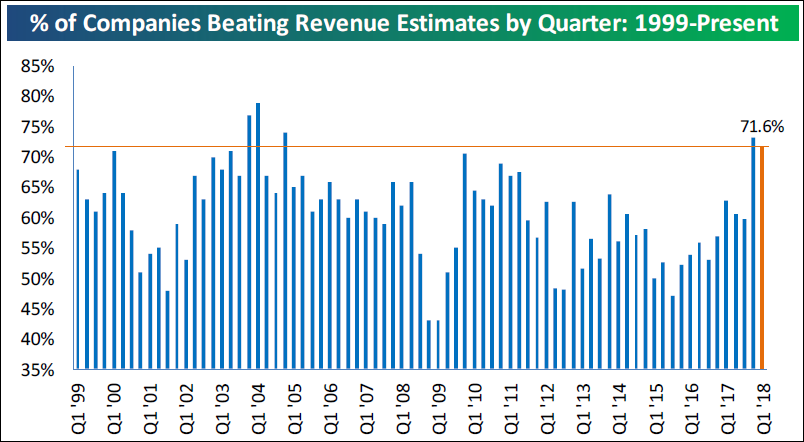

Also on the bullish side of the equation are earnings. It was a few years ago we opined the equity markets had transitioned from an interest rate-driven to an earnings-driven secular bull market, and the most recent earnings quarter did not disappoint. To be sure, the percentage of companies beating their estimates stands at 68.2% (Chart 2 on page 3), while the percentage of companies beating revenue estimates stands at 71.6% (Chart 3). Moreover, the spread between the percentages of companies raising earnings guidance versus those lowering guidance continues to expand (Chart 4). This is the mother’s milk of secular bull markets!

As our friend Jason Goepfert writes in his must have letter notes:

A breakout in breadth. The Cumulative Advance/Decline Line has made a new all-time high. Since 1940, that has led to a smaller chance of a large decline going forward, and a smaller average drawdown. When the S&P has lagged the A/D Line like now, it has been less consistent. We’re also seeing lagging breadth in the bond market.

As we wrote last week, “upside breakouts” are everywhere in the charts with many of the indices breaking out of symmetrical triangles. Leon Tuey highlighted this observation over the weekend when he wrote:

Also encouraging is that most market indices have broken out of the so-called “triangle” chart patterns that everyone was watching with bated breath. Moreover, they have broken above the moving average of the weekly Bollinger Bands. One of the theories of the Bollinger Bands is that when that happens, it will test the upper Bollinger Band. No wonder they all broke out of the “triangle” pattern. If the chartists have known this, they would have been certain that the market indices would breakout on the upside instead of sitting around picking daisy petals nervously.

Additionally, all our proprietary models are in upside breakout mode, despite the negative market pundits who continue to caution for a stock market crash. We continue to think the path of least resistance remains on the upside and continue to trade, and invest, accordingly.

The call for this week: During the entire month of January, we warned about the potential for a February Flop. That “flop” occurred right on time, followed by one of the most classic bottoming sequences we have ever witnessed, and we said so in these missives. Repeatedly, we have stated that we are treating the February 9, 2018 ‘undercut low’ at ~2533 as THE low until proven wrong and have recommitted the cash raised in January accordingly. As of last week, the D-J Industrials (INDU/24831.17) and the S&P 500 (SPX/2729.40) both have moved above their respective mid-April highs in what looks to be the completion of the bottoming chart formation that began in February. Importantly, those indices have seen a positive expansion in breadth. Stocks recording new highs are also suggestive of higher prices even though the stock market is overbought on a near-term basis. We think investors should focus on those sectors that are showing the greatest number of stocks making new highs: Energy, Financials, and Technology. The SPX futures are higher this morning (+6.00 points at 5:37 a.m.) as President Trump takes a softer tone towards China and Iran.

Chart 4

Source: Bespoke Investment Group

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|