By Jeff Saut, Chief Investment Strategist RJF, Tuesday 2 October 2018

“Nobody can consistently time the stock market’s ups and downs.”

. . . An old stock market “saw”

We have heard the statement, “Nobody can consistently time the stock market’s ups and downs;” and, for the most part we agree with that. However, if one listens to the message of the market, one can certainly decide if one should be “playing hard,” or not playing so hard. This view has to do with our often repeated statement about managing risk. As Benjamin Graham wrote in the book The Intelligent Investor, “The essence of portfolio management is the management of RISKS, not the management of RETURNS.” Graham closed that thought by noting, “All good portfolio management begins and ends with this premise.” We will note that our long, intermediate, and short-term models have done a better job than most of smoothing out many of the “wiggles” in the various markets. Accordingly, we were quite impressed with Leon Tuey’s latest missive, where he wrote:

There is a common belief that timing is not important and that no one can time the market. I beg to differ. Those who hold such beliefs are ignorant of the market’s logic. Also, it may well be just propaganda by the fund industry for if investors can identify a bull market top and pull their money out, what would the funds do for a living?

If investors understand the market’s logic, they can divine the future direction of the market (long-term, or shorter term). It is not rocket science. Understanding the market’s long-term direction is of primary importance. If investors had bought the following blue-chip stocks at the top in 2007 – Berkshire Hathaway, 3M, Microsoft, Royal Bank of Canada, United Technologies and hundreds ofothers, they would have lost 50% or more at the end of the bear market in March 2009 and they didn’t get even until early 2013.

To understand how a bull market begins and how it ends demands a deep understanding of the economic cause/effect relationships that drive the markets. The following must be clearly understood and appreciated.

The U.S. Federal Reserve System was created in 1913 to perform all roles monetary. It’s an independent body. One of its key statutory mandates is “To maintain orderly economic growth and price stability” (unlike the European model, which is primarily concerned with price stability). The most powerful tools at the Fed’s disposal to effect monetary policy changes are the basic monetary policy variables, bank reserve requirements, margin requirements, and the discount rate. Changes in the Bank Reserve Requirement and the Margin Requirement are infrequent; the discount rate changes the most frequently. When the Fed raises/lowers the Bank Reserve Requirement, however, investors should pay close attention as when it happens, it signals monetary tightening/easing. The single most bullish indicator for the stock market is when the Fed lowers the Bank Reserve Requirement; it’s a clear signal of monetary easing. To encourage investments, or to dampen speculation, the Fed will lower or raise the Margin Requirement. The Discount Rate is the only policy variable that changes frequently. Monetary tightening is when the Fed raises the Discount Rate many times in succession; drains liquidity from the system (contraction in the year-over-year rate of growth in the Adjusted Monetary Base, MZM, and M2. Data are available in U.S. Financial Data, reported every Thursday evening by the Federal Reserve Bank of St. Louis); and inversion of the Classic Yield Curve (13-week T-Bill yield vs. 30-year T-Bond yield).

The Fed’s mandate must be clearly understood and appreciated. Failure to do so will leave investors in a state of perpetual confusion and at the mercy of the “noise.”

To divine the market’s long-term trend, I monitor six factors to help me detect how a bull market begins and how it ends. These are the monetary (the most important and the real drivers of the market’s long-term trend), economic, valuation, sentiment, supply/demand, and momentum/internal/technical. The valuation and supply/demand factors are imprecise in terms of timing. Nevertheless, they must be closely monitored. The momentum/internal/technical factors don’t drive the market; they tell investors about the health of the market.

As mentioned on numerous occasions, if nothing else, if investors only understand and appreciate the following, they will always be on the right side of the market and will never be influenced by others’ opinions or news headlines:

IDENTIFYING A MAJOR MARKET BOTTOM

The bear market ends and a bull market begins.

IDENTIFYING A MAJOR MARKET TOP

The call for this week: We are on the West Coast seeing accounts, speaking at conferences, and doing gigs for our financial advisors and their clients. If past is prelude the markets will do something in our absence. Unsurprisingly, last week we received no less than 30 emails about the ten Hindenburg Omens that have been registered over the past two weeks (read: telegraphing a stock market crash). That indictor, however, is being triggered by the selling of interest-rate-sensitive ETFs and closed-end bond funds. Meanwhile, as we wrote last Friday:

“[Next] week we could see more powerful upside energy, but at this point it’s not looking all that powerful either. It’s more likely we’ll see more energy come into the market as we get closer to the [mid] November energy peak.”

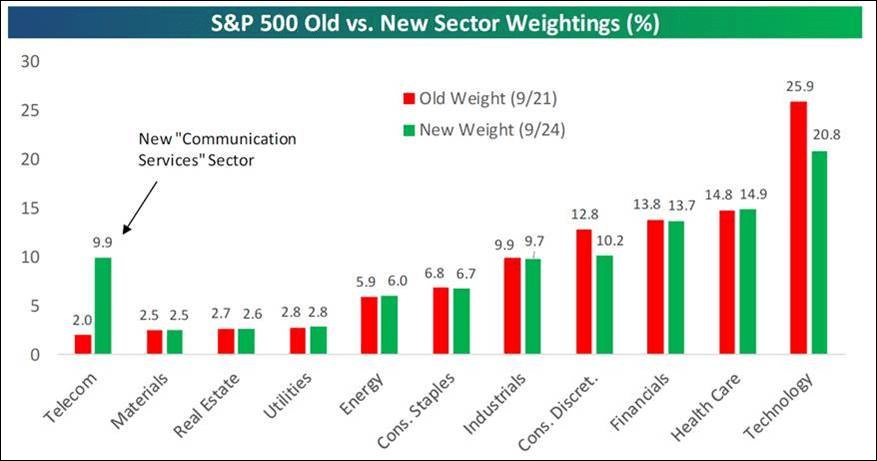

Quite frankly, given the low energy mix stocks typically “drift,” which is exactly what happened last week as we suggested. It may be more of the same this week, but should develop into something more powerful to the upside over the next few weeks. As a sidebar, the recent changes in S&P sector weightings are worth mentioning. Of particular note is that Telecommunication has gone from a 1.98% weight to a 9.9% weight (see chart below).

Yesterday, the equity markets caught an unexpected tailwind, although we have repeatedly said Canada was going to “blink” on NAFTA, and we think China will do the same. Evidently, the equity markets expect the same, but yet the equity markets could not hold on to yesterday’s gains into the closing bell. That is consistent with our upside “drift” call. Of our unpublicized letter yesterday, which is being published today, a day late, we stand by this strategy and embrace our upside trading target of 2980 – 3000 despite “calls” of this is JUST a range-bound stock market . . . GOOD GRIEF!

Chart 1

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|