In conjunction with our Terms of Business, the purpose of this policy is to demonstrate how Raymond James seeks to provide best execution for clients as required by the Markets in Financial Instruments Directive 2014/65/EU (MiFID II) and the Financial Conduct Authority’s Conduct of Business Sourcebook.

Best execution is the requirement to take all sufficient steps to obtain the best possible result when executing transactions on your behalf. Best execution takes in to account price, speed, likelihood of execution and settlement, costs, size and nature of the transaction or any other consideration relevant to the execution. Some of these factors will have a higher priority than others and the relative importance may alter when appropriate. Precedence will vary, since certain financial instruments trade within differing conditions and alter according to the order size and available liquidity. Raymond James generally considers price, likelihood of execution and settlement and overall cost to be of foremost importance but will factor in all these components when executing a trade.

Raymond James is obliged to provide best execution to all that use Raymond James for execution services. Raymond James will treat each trade with equal care and in accordance with this Execution Policy and the Order Handling Policy set out below.

To comply with the obligation to take sufficient steps to provide best execution and in addition to our London Stock Exchange access and member firm status, Raymond James has developed further electronic links to MiFID II compliant trading venues. These include a multi-lateral trading facility (MTF), an organised trading facility (OTF) and access to a high ranking systematic internaliser (SI). Additionally, further direct electronic connections have been established to access further execution venues. To ensure execution is best, Raymond James has also adopted a third party best execution tool to monitor execution trade by trade. Exceptions and outliers are initially reviewed at the time of trade and then by a supervisory second line on a periodic basis. Monitoring and reviewing in this manner allows Raymond James to identify any deficiencies and if any are found, corrective action can then be taken. Raymond James will review execution arrangements and our policy at least annually and whenever a material change occurs that might impact our ability to provide execution to the desired standards.

To ensure maximum asset class coverage and mid-price availability, Raymond James may execute all or part of your order outside of a trading venue when it is believed it is in your best interest to do so. In accordance with FCA requirements, consent will have been gained by your agreement to the Raymond James Terms of Business. This is particularly relevant for over the counter (OTC) trades. Furthermore and in line with the Raymond James Terms of Business, if Raymond James receives an investment instruction at a specified price limit with a specified size, i.e., a limit order, then it may not always be possible to execute that order under the prevailing market conditions. Raymond James would be required to make your order public unless you agree that we need not do so. Raymond James believes it is in your best interest that we exercise our discretion as to whether or not we make your order public.

Raymond James offers the following order types:

It may be the case you or your wealth manager decide to include a specific instruction to part or all of an order. By following a specific instruction, Raymond James will have satisfied the obligation to provide you with best execution in relation to the relevant part of the transaction to which the specific instruction applied. Examples of such instructions include, but not limited to, a change in standard settlement timeframes or settlement centre, order types other than market (e.g. limit), or directed trades to a particular counterparty or venue (please note that this could be by selecting a security identifier away from the primary listing).

Raymond James may use connected parties for execution in North America only and only in accordance with this policy. Please note, when directly using a connected party or third party custodian for execution, it is that third party’s best execution and order handling policy that will apply to all orders not executed by Raymond James. For investments held with Raymond James and Associates, details can be found here.

This Execution Policy applies to times in the normal course of business. When necessary or in times of distressed and abnormal markets, Raymond James reserves the right to vary any aspect of the Execution Policy without notice. Raymond James also reserves the right to aggregate like client orders when appropriate to do so.

This Order Handling Policy is designed to outline how Raymond James treats orders after live submission to the Raymond James dealing desk. In the first instance, Raymond James will look to aggregate like market orders for speed, efficiency and in order to ensure that clients obtain the best outcomes. The intent is to provide a uniform price for all like orders and to prevent a proceeding order impacting the price for any subsequent orders. Following aggregation, for securities that normally trade on a regulated market (RM) and based on pre-determined criteria, a rules engine within our order management system (OMS) will decide where to route the order to consistently obtain the best outcome. For market orders that are within the normal market size (NMS) of that security, a retail electronic quoting system is employed. This is known as the Retail Service Provider (RSP) and accesses a range of competing market makers or eligible counterparties to seek the best price for execution. For orders outside of the normal market size, routing will depend on the security type. For liquidity seeking purposes, Raymond James reserves the right to route orders through brokers or agents when appropriate.

Where Raymond James requires the use of brokers or agents to access markets, Raymond James will ensure a best execution obligation is in place and that periodic reviews occur to measure and monitor execution quality. Raymond James may choose to execute client orders by using direct electronic access services provided by third parties when it is deemed the most effective way to execute the order. Direct electronic access may employ the use of algorithms that intelligently seek the best price and liquidity across a wide range of venues. The algorithms are designed to only take the best price irrespective of venue with the objective of ensuring quality and certainty of execution. Raymond James will not discriminate against execution venues other than when access is restricted or not readily available or compatible with our OMS. The most appropriate venue will be selected based on the relative features of the trade and the corresponding class of asset.

For international and larger equity trades, Raymond James has direct market access to the London Stock Exchange, electronic links to global systematic internalisers, registered market makers and brokers with further reaching venue and liquidity access. As a London Stock Exchange member, Raymond James can also negotiate on venue execution with fellow member firms, eligible counterparties and brokers.

For larger equity and equity like orders, particularly exchange traded products (ETPs), orders may route to a multi-lateral trading facility that employs a request for quote model that will quote a selection of authorised participants (AP’s) and liquidity providers. These entities then disclose their best quotes enabling the best price to win the trade, all within a further set of predetermined best execution rules.

For debt instrument trades, orders may route to an organised trading facility or multi-lateral trading facility to obtain request for quote functionality. There may also be instances where liquidity constraints require Raymond James to use agency brokers. The use of agency brokers will be limited to those that operate their own organised trading facilities or can assist in trade reporting, while sufficiently evidencing best execution.

For bespoke products or other allowable securitised derivatives, Raymond James will endeavour to trade at the best price. Best execution with assets of this nature is usually implicit since there is typically only one available price for trading and one execution venue.

The execution process for trades placed in collective funds where the fund manager is the only destination are not captured in this regulation.

MiFID II: Directive 2014/65/EU of the European Parliament and the Council on Markets in Financial Instruments and any implementing directives and regulations.

Trading Venues: Financial instrument exchanges that are categorised as one of the following: Regulated Market (RM), Multi-lateral Trading Facility (MTF), Organised Trading Facility (OTF), or Systematic Internaliser (SI).

Execution Venue: Trading venues plus market makers or other liquidity providers or entities that perform similar functions for trading in a third country. Examples that are not trading venues but are execution venues and accessed by Raymond James are Stifel Nicolaus Europe Limited, Winterflood Securities Limited, Instinet Europe Limited and Peel Hunt LLP.

Regulated Market (RM): A Regulated Market is a multi-lateral system that facilitates the bringing together of multiple market counterparties where buying and selling financial securities occurs and results in a binding contract. Examples include the primary global exchanges such as The London Stock Exchange, Deutsche Boerse Xetra, The Hong Kong Stock Exchange and the New York Stock Exchange.

Multi-lateral Trading Facility (MTF): A Multi-lateral Trading Facility is any system or facility operated and/or managed by an investment firm in which participants can buy and sell financial securities by interacting within the facility. Examples include: Tradeweb MTF and Bloomberg MTF.

Organised Trading Facility (OTF): An Organised Trading Facility is a multi-lateral trading facility operated by an investment firm or a market operator. It allows trading in non-equity instruments. MiFID II does not permit trading of equities on an OTF. Examples include: Tradeweb OTF and GFI Securities OTF.

Systematic Internaliser (SI): A Systematic Internaliser is an investment firm, which, on an organised, frequent, systematic and substantial basis, deals on its own account when executing client orders. These orders are executed outside of a regulated market, MTF or OTF but are MiFID II compliant and regulated. Examples of firms operating as an SI for certain security types include Morgan Stanley, Societe Generale and HSBC.

Over the Counter (OTC): Over the Counter or off-exchange trading are transactions directly between two parties and not under the rules of any trading venue. By accepting the Raymond James Terms of Business, permission has been given for Raymond James to engage in OTC trading when it is considered to be beneficial to the client.

Order Management System (OMS): An Order Management System is an electronic system developed to execute securities orders in an efficient and cost-effective manner. Brokers and dealers use these when trading various types of securities.

Order Blocking and Merging (OBM): Order Blocking and Merging is the process of aggregating like orders. This may be automatic or manual.

Normal Market Size (NMS): Normal Market Size is a number of shares categorised as the size of a transaction that is normal for a particular security and obliges registered market makers to deal within these sizes at the prevailing primary market price.

Authorised Participant (AP): Authorised Participants are generally the major liquidity providers at the centre of the exchange traded products (ETP) creation and redemption mechanism. As such, authorised participants play a critical role in ETP liquidity.

Exchange Traded Products (ETP): Exchange Traded Products are defined as ‘equity like’ under MiFID II since they can trade continuously on an exchange during market hours. Among others, Exchange Traded Products encompass; ETF’s (Exchange Traded Funds), ETC’s (Exchange Traded Commodities) and ETN’s (Exchange Traded Notes).

Direct Market Access (DMA): Direct Market Access is trading on a regulated market using an investment firms own membership. Where membership of the market is not appropriate, DMA can be achieved through use of a broker or similar third party.

Retails Service Providers (RSP): The Retail Service Providers are a collection of market makers or counterparties that will make prices in listed securities that Raymond James can poll to obtain a best price. Market makers participating in this electronic trade execution system as at 11 September 2024 include:

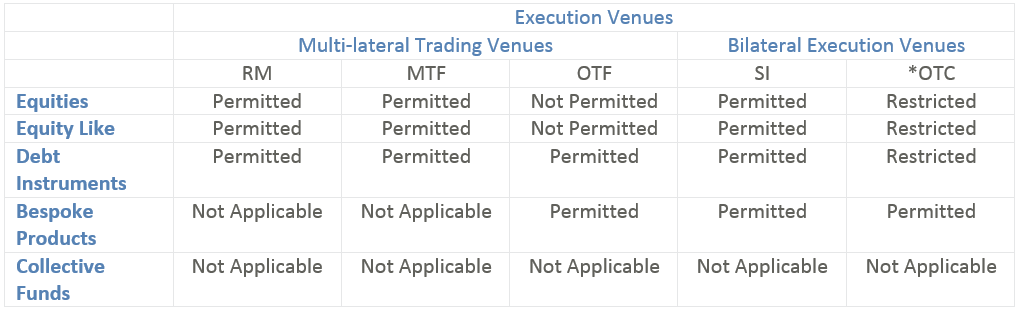

European and UK regulation from 3 January 2018 covers additional asset classes to the previous regime and seeks to bring as much trading on venue as possible. Below is a summary of asset classes and the available venues for trading.

*OTC execution is restricted from 3 January 2018. Certain asset classes may not be available to trade on a particular venue but may have the characteristics of a similar asset class that does. Where trading on a venue is unavailable, OTC is permissible when prior client consent has been sought.

Additional regulatory information can be found under the FCA website www.fca.org.uk and the ESMA website www.esma.europa.eu.

Page last updated 12 September 2024

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|